The Biopharma A List: Taking The Pulse Of Newco Creation

Executive Summary

On the new company creation front, using Series A financings as a proxy, start-ups have not escaped the challenging funding environment. Here we update trends in those first-time rounds for 2023.

Biotechs have faced challenges in the last couple years on many aspects: achieving clinical and regulatory milestones, appeasing investors whom are less willing to take risks on early-stage assets, and a buyer’s market in favor of pharma dealmakers. Public markets have been difficult to reach in the last 12 months as well, and for venture capitalists, raising new funds has been a struggle.

Series A financings remain a strong component among all venture funding for biotechs. On average, over the last 7 years, Series A rounds account for just over one-third of annual venture capital (VC) funding (see Exhibit 1). However, the shrinking pool of funding in the industry has resulted in a gradual year-over-year decrease in the proportion of Series As as a total of all VC financing. In 2023, the sector reached a low of 29% of the VC financing group represented by first-time fundraisers.

New Company Creation Slows Down

The number of new companies being formed, at least based on Series A activity, has been slowing down (see Exhibit 2). After reaching a five-year high of 200 transactions in 2021, Series A volume has been declining over the last 2 years, decreasing by 19% to 162 from 2021 to 2022, and by a substantial 40% from 2022 to 2023, during which just under 100 start-ups received Series A money, almost the smallest number seen aside from 2019’s close figure of 96.

Aggregate amounts of Series A funding have fluctuated in recent years. Despite 2022 appearing to feature a peak of $10.6bn, it is important to note that $3bn of that came from one financing, Altos Labs’ emergence from stealth mode to fund its work in cellular rejuvenation. The company, founded by GlaxoSmithKline PLC veteran Hal Barron, has stayed quiet and not made any public announcements since their January 2022 launch. (Also see "Big Names Backers Give Altos $3bn To Pursue Cell Rejuvenation Science" - Scrip, 19 Jan, 2022.) Excluding that outlier, the industry is also witnessing a decline in total Series A values since 2021, and in 2023 the total dropped down to $6.1bn – although not the lowest amount seen during 2017-23 time period.

More Companies Raising Larger Rounds

The average haul a start-up brings in has been rising year-over-year (see Exhibit 3). In 2023, the mean A round size was $63.6m, just slightly behind the high of $66.4m from the previous year. In the last 5-6 years, an average Series A financing has totaled at least $50m, and this is nearly double the average size reported in 2017. Even excluding Altos’ mega round in 2022 only brings the average for that year to about $48m.

The increasing average round size makes sense, as the industry is seeing a shrinking proportion of companies completing first-time financings of $10m or less (see Exhibit 4). In 2017, about one-quarter of start-ups did an A round in this category, but by 2023, that number dropped to only 7%. Instead, rising proportions of companies are closing rounds in the >$50m-100mrange. In particular, 2023 saw more financings done between $200m-300m than in recent years.

2023 Series A Financings In Focus

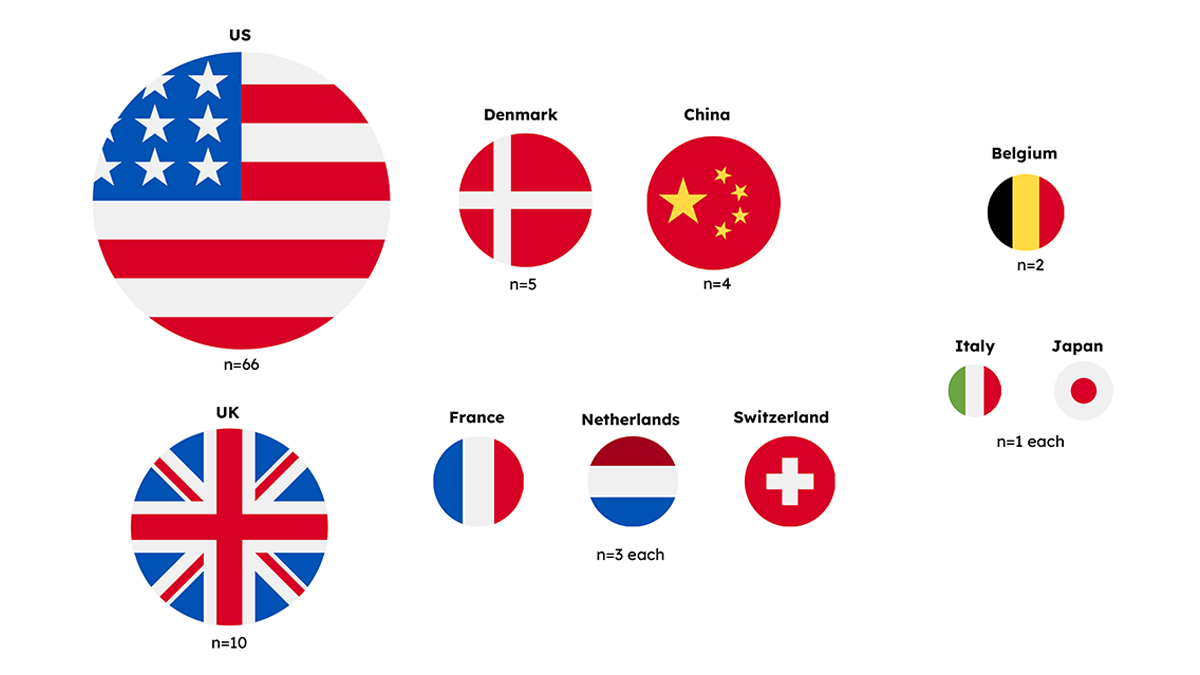

The top 10 Series A rounds from 2023 spanned companies working in multiple therapy areas and novel technologies (see Exhibit 5). This leading group featured financing totals ranging from $142m up to $315m at the highest end. In the top 3, the industry saw Hasten Biopharmaceutic building its CV-met portfolio [See Deal], plus two companies, ReNAgade Therapeutics [See Deal] and Orbital Therapeutics [See Deal] focused on RNA development. Representing the largest Series A of 2023, Hasten is based in China, where only three other start-ups were located that completed A rounds. ReNAgade Therapeutics and Orbital Therapeutics, rounding out the top two, are both US companies; the US is where two-thirds of the Series A start-ups (66 out of 98) were headquartered in 2023 (see Exhibit 6).

Hasten Gets Big Investment from CBC And Mubadala

Hasten, a 2020 start-up, is building a portfolio of products in the cardiovascular, metabolic and critical care spaces through product acquisitions from big pharma. Its recent Series A investment will help to continue expanding those offerings. The company brought in $315m through its Series A financing, which CBC Group and Mubadala Investment Company co-led and were joined by institutional investors. The majority of Hasten’s marketed drugs came from a 2020 deal with Takeda Pharmaceutical Co. Ltd. worth $322m. [See Deal] In that agreement, Hasten picked up Chinese rights to the antihypertensives Ebrantil (urapidil), Blopress/Atacand (candesartan cilexetil), and Edarbi (azilsartan medoxomil), plus the diabetes medications Actos (pioglitazone) and Basen (voglibose). These were deemed non-core assets by Takeda, which at the time was selling off multiple products as a result of its Shire acquisition. More recently, Hasten has boosted its portfolio through licensing transactions for Chinese rights to antibiotic Rocephin (ceftriaxone) from Roche Holding AG and to PCSK9 inhibitor lerodalcibep from LIB Therapeutics, LLC.

ReNAgade Addresses Targeted RNA Delivery With Novel Lipid Nanoparticles

Overcoming challenges, particularly targeted delivery, of RNA medicines, is critical for commercial success of this promising modality. ReNAgade is trying to do just that. The firm launched with a $300m Series A round in which MPM BioImpact and F2 Ventures were the lead investors. (Also see "ReNAgade Emerges With $300m To Pursue Extra-Hepatic Delivery Of RNA Medicines" - Scrip, 23 May, 2023.) The money will support its key goals in developing an integrated RNA platform – to deliver, code, edit and insert RNA, addressing specifically targeted tissue delivery anywhere in the body using proprietary novel lipid nanoparticles. The company has presented preclinical data on delivery of mRNA in extra-hepatic tissue. The coding aspect of ReNAgade’s platform will be the focus of a joint venture with Orna Therapeutics, Inc., which brings its circular RNA technology to the partnership. Orna’s technology aims to improve expression in reprogrammed cells, allowing for earlier validation of any programs ReNAgade wishes to advance. These technologies will also be part of a deal between Orna and Merck & Co., Inc., which will work on therapeutics and vaccines in infectious diseases and oncology.

Orbital Looks To Extend Durability

Also focusing on the RNA sector is Orbital, which completed a $270m Series A financing from lead backer Arch Venture Partners and multiple other investors. Like ReNAgade, Orbital is building a platform encompassing multiple aspects including delivery methods, data science, and automation. Orbital was established in 2022 and began operations with a cross-licensing agreement with base gene editing company Beam Therapeutics Inc., in which the companies swapped RNA and non-viral delivery technologies. Orbital will focus broadly on RNA medicines outside of siRNA. The start-up’s mission is to extend the durability and half life of RNA therapeutics, and to reach a broader range of cell types and tissues. Its first target areas of interest will be vaccines, immunomodulation, and protein replacement.

Arch, OrbiMed And Eli Lilly Were The Most Active Series A Investors

In 2023, just over 300 unique investors backed start-ups in their Series A rounds, ranging from traditional venture capitalists, pharma and biotech companies or their corporate venture capital (CVC) arms, and even academic centers. Among traditional VCs, Arch Venture Partners and OrbiMed tied as the most active Series A investors in 2023 with nine rounds each (see Exhibit 7).

Notably, about half of the Series As Arch was part of were worth $100mor more. Arch was the lead investor on the largest of those, in which RNA player Orbital Therapeutics brought in $270m in financing. OrbiMed co-led three of its nine Series A financings, including syndicating with RA Capital Management for Convergent Therapeutics ($90m) [See Deal], with Jeito Capital for Corteria Pharmaceuticals ($72m) [See Deal], and with Qiming Venture Partners for Epigenic Therapeutics ($32m). [See Deal]

For large industry players, buying stock in an emerging company allows for an early view into novel technologies. For Eli Lilly and Company, this was especially the case in 2023 as the big pharma participated in a total of nine Series A financings. Nido Biosciences’ combined seed, Series A and Series B financing was the largest Lilly participated in, with the round totaling $109m support development of precision medicine small molecules initially for amyotrophic lateral sclerosis (ALS) and frontotemporal disorders. Neurological disease start-ups were a particular focus for Lilly, which also invested in the Series As of RNAi company Switch Therapeutics, raising $52m and fibrin-targeting Therini Bio, Inc., taking in $36m. Advanced therapies and related technologies were also of interest to Lilly; besides Switch Therapeutics, the Big Pharma joined in the A rounds for DiogenX, which is developing a recombinant protein that regenerates insulin-producing beta cells to treat diabetes; and for ViaNautis, whose polyNaut platform aids in targeted delivery of pDNA, mRNA, siRNA and antisense oligonucleotides. Following Lilly’s nine total Series A investments, the next most active pharmas – either the companies themselves or their CVC arms – were Bristol Myers Squibb Company, MRL Ventures, Novartis Venture Fund, Pfizer Venture Fund and Sanofi Ventures, at three investments each.

Oncology, Including Radiopharmaceuticals, Draws Most Series A Funding

Among the largest Series A rounds – those worth at least $50m or more – oncology dominates as the therapy area of focus for start-ups (see Exhibit 8). A total of 17 companies working on cancer drug development completed first-time financings in 2023, together bringing in $1.3bn (note that start-ups involved in more than one therapy area are counted multiple times in each relevant area). Leading this pack was CARGO Therapeutics, which received $200m in a round co-led by Third Rock Ventures, RTW Investments, and the Xontogeny Venture Fund. [See Deal] Founded by scientists from Stanford University Center for Cancer Cell Therapy, CARGO is currently in a Phase II trial with its autologous CD22-targeting CAR-T cell therapy CRG-022 for large B-cell lymphoma. Several months after the A round, CARGO completed an IPO worth almost $300m. [See Deal]

Within oncology, radiopharmaceuticals garnered attention, accounting for 3 of the 17 start-ups that completed big Series A financings. Abdera Therapeutics closed a combined Series A/B of $142m, while Convergent Therapeutics and ARTBIO each raised $90m. The area has gained M&A buzz in the last several years, including most recently in large deals by Bristol Myers Squibb (acquiring RayzeBio, Inc.for up to $4.1bn) and Eli Lilly (buying POINT Biopharma for $1.4bn). In the overall radiopharmaceutical pipeline, there are at least 7 promising Phase 3 programs advancing through development currently in prostate cancer, GEP-NETs, and other cancers. (Also see "What’s New, And What’s Coming, In Radiopharmaceuticals" - Scrip, 2 Feb, 2024.)

Development of advanced molecular therapies by the biggest first-time fundraisers was also a key theme in 2023. About one-fifth of the companies (10 or the 47 unique companies that raised ≥$50m) are involved in the fields of cell, gene or RNA therapies. Notably, many of these start-ups are concentrating mainly on overcoming challenges with delivery of these types of molecules. Besides ReNAgade and Orbital, Aera Therapeutics has a proprietary protein nanoparticle platform of endogenous, human proteins derived from retroelements that can self-assemble to form capsid-like structures that transfers nucleic acids; Aera launched with a combined $193m in Series A and B financing. And Rampart Bioscience brought in $85m in Series A funds to support work on HALO, a technology that designs DNA medicines with certain structural elements that avoid issues with gene therapy potency, durability and re-dosing.

Looking Ahead

The last couple years indeed have been challenging in the biopharma industry, but there are signs of optimism. At the industry’s bellwether event, the J.P. Morgan Healthcare Conference, at the start of 2024, the mood was positive and big M&As and partnerships were abound – a signal that M&A itself might rebound after falling in 2023. (Also see "J.P. Morgan 2024: Optimism With An Undercurrent Of Tension" - Scrip, 10 Jan, 2024.) And recent data from financial firm Silicon Valley Bank points to a healthy amount of fundraising by US venture capital firms totalling $19bn in 2023, which bodes well for future start-ups aiming to fund promising science.